Surfactants Monthly - June 2024

June 2024 Surfactants Monthly

Promos:

Check out our event page here (https://www.neilaburns.com/events/10th-asian-surfactants-conference ) for the great return to Asia for the 10th Asian Surfactants Conference. We’ll be in Kuala Lumpur, November 19 – 21, with the original surfactant business essentials course Tuesday 19th and the conference November 20th – 21st. This is our first time in Malaysia for the conference – long overdue. The lineup of speakers and partners is already incredible. We’re at the legendary ParkRoyal Collection Hotel in the heart of Bukit Bintang. Please book early to ensure attendee rates at the hotel. This promises to be our biggest and best Asian event yet.

Big In Malaysia

The News

A crazy amount of news this month, so let’s get to it.

Macroeconomics: More from Nomura. Chemicals and materials M&A running behind for the first five months of the year – 31% on deal volume, 56% on value. Why? I can only speculate. Pre-election(s) jitters maybe. Nerves re the economy (see Evercore data later)

I-Bankers spending more time on the beach?

Having said that, the IPO market is picking up

Coming back…

Mid-June Macro notes from Evercore conclude essentially that The US economy remains strong but shows signs of slowing and that Evercore ISI US company surveys, which are in nominal terms, declined to below 50, into the “Struggling” zone [sounds awful]. Nominal consumer spending, nominal wages & salaries, and nominal bank deposits/loans also suggest slowing.

Chemical inventories are back to normal – great. I’n hearing that.

But trucking seems very weak. I have not heard that – what about others? It seems not a good sign right? What are you seeing out there. Canary? Coalmine?

Not looking great…

?

BTW: Our readers are really smart. A long time reader of the blog and member of our industry had some interesting comments on last month’s discussion of specialty chemical vs commodity EBITDA multiples. He (or she!) wishes to remain anonymous and so here are my paraphrasings of some of her (or his!) key points. :

Companies with low P/E multiples means the market thinks the earnings are about to get torched.

A company like [name withheld so I don't get angry emails], with a commodity business and relatively low EBITDA multiple, can never predict when their earnings might soar or crash. It is often due to a sudden realization by the market that supply and demand are out of balance and there is nothing management can do about it except accept the price consequences. Earnings could fall 50% in one year, which is not uncommon in commodity cycles. That risk of price change is what the market discounts. It is the same for oil companies.

Specialties create some performance or sensory value and have by definition some 'moat' around de-formulation or substitution by an identical molecule. They are usually a mixture of molecules instead of pure, like ethylene. Formulators are not always 100% sure why something works (meaning both molecule mix and source) so they don't want to change it until cost pressure becomes extreme. Hence specialty companies like [name also withheld] enjoy higher trading value in the market.

Our reader went through many commodity cycles and recalls trying to explain same to I-Bankers. Ultimately, in their opinion, you can't convince anyone that management has any influence over pricing, just over cost control and capacity loading. If those are fairly well optimized, then the price swings make all the difference. Managers will often claim that price increases were due to marketing genius and declines due to stupid competitors, In reality, everyone just wants to run their factories at full tilt since that is the best you can do in a given market condition. Market shares tend to equal capacity shares.

Provocative stuff! What say you?

Our readers are smart

Also, courtesy of Nomura, some M&A and financial news that I have cherry-picked here to include those that could be said to have some surfactant relevance. Dig in deeper obviously to those of particular interest.

· On May 7, Turnspire Capital Partners, a private equity firm, acquired the nutraceuticals business of Ashland, a provider of nutrition ingredients and custom formulation services that supply active and ingredients and formulation aids

· On May 8, Dorf Ketal Chemicals, an India-based specialty chemicals manufacturer, acquired Impact Fluid Solutions, a specialty drilling and workover fluid additives company

· On May 15, Insempra, a technology company developing sustainable ingredients, raised $20mm in Series A funding with participation from EQT Ventures, BlueYard Capital, Possible Ventures, Taavet Sten and Acequia Capital amongst others

· Other News: Verbio, a Germany-based company producing and distributing biofuels, commenced the construction of the world’s first large-scale ethenolysis plant at Bitterfeld, Germany to manufacture bio-based specialty chemicals for detergents and cleaning agents . If you read the press release, you’ll see that this is similar to what Elevance tried with their refinery in Malaysia with Wilmar. The release notes that methyl 9 decenoate is a component of detergents and cleaning agents but ECHA notes here that is important and manufactured in the EU at only between 10 and 100 MT per year. So – I don’t know. Let’s see I guess.

What’s going on with Chemical Distribution?

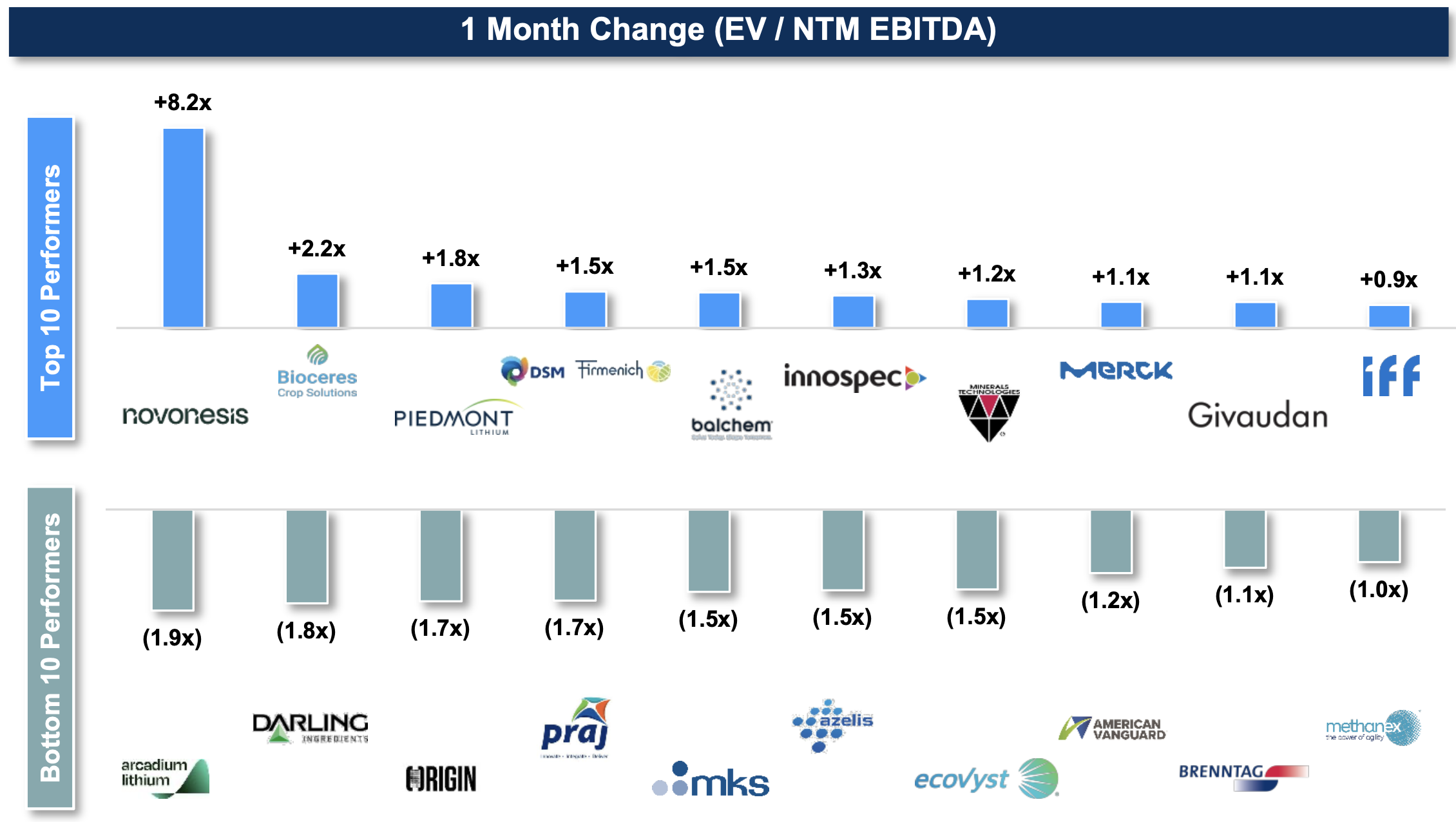

Nomura has a neat chart showing the last months change in trading EBITDA multiples for chemical relevant stocks. Some familiar names in the top 10, including 3 fragrance companies. But what’s the deal with the bottom 10 with Azelis and Brenntag? More canaries in the coalmine? Readers – please comment if you like.

Brenntag and Azelis stocks had a rough month.

Our friends at Galaxy Surfactants reported their FY 2024 results at the end of March. Some key points:

· Sales at 3,794.4 crore Rupees (that $454.2 Million) are down 15% since last year, despite volume growth of 7.7%.

· EBITA also down 14% at 497.7 crore Rupees ( $59.6 Million).

KLK (Kuala Lumpur Kepong Berhad) one of the big Malaysian palm oil companies with significant downstream activities in surfactants, particularly in Europe and Asia reported 2nd quarter earnings. Bottom line, the plantations are doing well but what they call manufacturing, mainly oleochemicals, not great – but the worst is behind them. Here’s a snapshot of 6 months YTD vs 2023 (as of 3/31). Note that the there are 4.7 Ringgits to the USD.

KLK Results 6 months

The company commented (and I quote almost verbatim):

Plantation

Despite realised CPO selling price was flat at RM3,470/mt ex-mill (4QFY2023: RM3,476/mt ex- mill), Plantation profit was 11.3% lower at RM370.4 million (4QFY2023: profit RM417.5 million) mainly due to:

- Higher cost of CPO production.

- Fair value loss of RM9.5 million (4QFY2023: gain RM33.9 million) on valuation of unharvested fresh fruit bunches.

However, the decrease in profit was cushioned by higher CPO and PK sales volume coupled with better PK selling price realised at RM1,800/mt ex-mill (4QFY2023: RM1,743/mt ex-mill).

Manufacturing

Despite revenue declined by 6.0% to RM4.477 billion (4QFY2023: RM4.765 billion), Manufacturing segment returned to a profit before tax of RM25.3 million (4QFY2023: loss RM102.1 million) mainly due to higher profit reported by refineries and kernel crushing operations and lower loss from the Oleochemical division.

Regarding the prospects for the oleochemical business, the company notes that the Oleochemical sub-segment reported weak results with a loss of approximately RM9.3 million amid sluggish demand, high interest rate environment and ongoing geopolitical tensions impacting global trade. The Group experienced marginal increase in sales volume in the reporting quarter with eroded margins. The Group sees stronger demand in Europe and Southeast Asia for 2nd quarter of FY2024.

We occasionally write about agricultural adjuvants in these pages. If you’re interested in this area, I encourage you to get hold of a copy of the latest Agropages publication on formulation and adjuvant technology. It’s free. Among the familiar names featured in there are Clariant, Nouryon, Evonik, Croda, Indorama (former Oxiteno), Ajinomoto (surprised me), Ingevity, IMCD and Ingevity.

Agriculture continues to be attractive

More Regulations: A reader drew my attention to a New York State Assembly Bill # A6969B called in short “the beauty justice act” and further defined as a “AN ACT to amend the environmental conservation law, in relation to the regulation of ingredients in personal care products and cosmetics” Ugh – so what is it about. The act references an NIH study, that found that women of color who regularly used dyes and straighteners had a 45 percent higher breast cancer risk. White women faced a 7 percent higher breast cancer risk. OK – the bill’s aims seem noble enough but the list of restricted substances is a bit of a head-scratcher. It contains Ethylene Oxide (CAS # 75-21-8) – (Yes I checked it. That’s EO). So what does this mean? No one is adding EO to their hair treatments. Ethoxylates of course, yes. Will this be realized and someone try to amend it to ethoxylates. Apparently the bill already went through state senate review. Any reader know any more on this one? To me, it’s not a good look for regulators.

Had enough regulation yet?

More on chemical distribution. Univar is privately owned and so we don't know what the market would think of recent moves (see Brenntag and Azelis notes above), but it’s worth noting that Univar now goes to market as three business units incorporating the six prior focus industries – Care (home & industrial cleaning, and beauty & personal care), Performance Materials (CASE, lubricants and metal-working fluids), and Health & Nutrition (food and pharmaceutical ingredients). In an interview with ICIS, Nick Powell, president of global ingredients and specialties said that after a difficult stretch of around 18 months through the end of 2023 for the chemical industry, Univar saw a rebound in Q1 2024 which is running through much of Q2 thus far. “Q1 was very good for us. If we were to compare our results against some publicly traded pure play competitors, our results would stack up very favorably. We believe we’re taking share, and volumes are growing nicely,” said Powell. He added “I think destocking is over and supply chains are empty. What we see now is customer demand flowing very quickly through to producers or to distributors. That’s the effect we’re seeing year-to-date – an uptick versus where we were 12 months ago,” OK so fine, but I cant quite get over that Evercore data above. Comments?

Stepan has published a 2023 sustainability report. It’s a pretty nice document. You can check it out here. https://www.stepan.com/content/stepan-dot-com/en/sustainability.html Take a look at page 30 which lists some of the organizations of which they are a member.

We love new surfactant announcements. Premium Beauty News reports that Kaffe Bueno launches a new anionic surfactant – Kleanstant. While I’m not crazy about the name, especially for a cosmetics ingredient, it sounds interesting. The company is from Denmark and According to Kaffe Bueno, the new ingredient harnesses the beneficial properties of coffee oil, offering a sustainable alternative to conventional surfactants, like Sodium Lauryl Sulfate (SLS). It contains potassium salts of palmitic and linoleic acids, polyphenols, tocopherols, and diterpene esters, delivering effective cleansing, emulsifying, foaming, and antioxidative properties. Kleanstant can be used to easily remove waterproof make-up without drying the skin. Naturally rich in antioxidants it protects the skin while leaving a soft and smooth feeling on the skin. However, this versatile ingredient is also suitable for cleansers, soaps, shampoos and body washes at a dosage comprised from 5% to 40%. If anyone has used it, please let me know what you think. BTW More recently, Givaudan launched Koffee’Up. Marketed as an alternative to argan oil, the upcycled ingredient is made from spent coffee grounds. The ingredient has been developed in partnership with you guessed it - Kaffe Bueno.

Coffee is good for you

More on Tide Evo? HAPPI magazine reported on P&G patent regarding a Multilayer Dissolvable Solid Format Product. It’s this one https://patents.justia.com/patent/12018232 . Most likely one of the patents behind the fascinating Evo (any users want to report their experience with it?)

Dall-E puts Tide Evo into the KL Cityscape (obviously been spying on me)

We don’t often write about them but, Covestro, a polyols producer announced it had entered into “concrete negotiations” with Abu Dhabi National Oil Co. (Adnoc) over a potential takeover bid from Adnoc that could value Covestro at almost €12 billion.The starting point for the talks is a possible offer price indicated to Covestro by Adnoc of €62 per Covestro share, it said. This would value Covestro at about €11.7 billion. The offer price is subject to the results of the confirmatory due diligence, and agreement on the content of an investment agreement, Covestro said. Covestro also announced a global efficiency program to cut €400 million in annual costs by the end of 2028, with the savings to come from “material and personnel costs,” it said. About €190 million of the total cost cuts will be implemented in Germany, it said. Of course, the other big company with an Abu Dhabi link is CEPSA whose 63% owner is Mubadala fund.

More new surfactants news. In a June 11 interview with Indian Chemical Weekly, Rajesh Kamat, Head - Sales and Marketing, Tata Chemicals, noted the company is working on new biobased surfactants. Unfortunately, that’s all that was said about it in the long interview. Hmm – from their annual report, I was able to pick up the following: “Our Innovation Centre has developed bio-based surfactant from agri waste, using Green Chemistry principles. Used as an ingredient in detergents, this bio-based surfactant will be a sustainable alternative to non-biodegradable surfactants. This patented product has proven to be biodegradable, non-skin irritant, and non-flammable during ongoing trials.” We’ve been in touch with the company to see if we can get more. Agriculture and it’s associated waste is a big deal in India.

In a June 14, article in The Cooldown, we learn that This spring, Tide and Walmart joined forces to show customers firsthand how switching to a cold water wash can help save shoppers up to $150 every year while reducing energy consumption by up to 90%.

Tide has also teamed up with Electrolux, GE, and Samsung to literally build the change into washers, with an innovative feature that claims to enhance the machine's ability to wash on cold. Readers of this blog, smart as they are, already know that the biggest carbon footprint impact in the surfactant value chain is made at the consumer end – un use. Todd Cline, P&G’s director of sustainability goes on to explain :

"About 70% of the carbon footprint of doing a load of laundry is not driven by the raw materials, the packaging components, [or] the manufacturing," Cline said. "It's actually how the consumers use the product. And it's whether someone chooses hot, warm, or cold when they're picking their temperature.

• Switching from hot to cold -> 90% reduction in energy on average.

• Switching from warm to cold -> 70% reduction in energy on average.

Cool is hot in laundry (sorry!)

Here’s a neat (and serious) video explainer:

I often get asked the question – why can’t we use longer or shorter chains than 1214 in surfactants – and what happens if we try? And honestly, I’m never quite happy with my answers. So I am happy to see that Nancy Falk, formerly of Clorox and now an independent consultant (and by the way who has spoken at one of my conferences) has written an outstanding article in the journal of surfactants and detergents called “Impact of non-palm triglyceride feedstocks on surfactant properties and consumer product applications” Check it out here. It clocks in at a crisp 8 and a bit pages including references. Worth a read and further study (you know who you are).

And finally (in the news), Syensqo announced a partnership with Allozymes, an enzymes company. The press release reads, in part: Syensqo and Allozymes, a Singaporean enzyme engineering start-up, announce the signing of a Memorandum of Understanding (MOU) to leverage both companies strengths in biotechnology towards the development of advanced biosolutions for Home and Personal Care, in particular for the skin care market. Allozymes stands out in the bio-engineering sector with its unique ultra-high throughput microfluidics platform for the engineering of enzymes and microbes. This platform enables the rapid and cost-effective development of biomanufactured ingredients and bioprocesses, setting a new standard for innovation and sustainability in the industry.

“By combining Allozymes technological capabilities with Syensqo's application and market access expertise, we are poised to create groundbreaking solutions that will not only benefit the home and personal care market but also contribute to a more sustainable future.” This MOU marks an important milestone in Syensqo’s strategic agenda of rapidly expanding its beauty specialty ingredients portfolio based on biotechnology. It complements the company's recent acquisition of South Korean ceramides specialist JinYoung Bio, further solidifying its commitment to enabling sustainable and innovative care solutions.

Lot more to learn about enzymes

Now to the market news:

LAB and LAS:

The US market saw a slight increase in price for LAB to around USD 2,090 per MT . Prices in the rest of the world were mixed and remained below that in the US as is usually the case.

Spot prices for LAS in Asia up slightly to – USD 1,270 – 1,360 per MT

Ethylene, EO and Ethoxylates:

EO in the US: Prices remain steady at 57 – 59 clb

EO in the EU : Steady at around 1,495 per MT.

In Asia, Ethoxylates nudged up to USD 1,500 – 1,600 per MT.

Detergent Range Alcohols:

Reminder. We’re talking here about alcohol’s in the carbon chain length range 12 – 18, regardless of provenance – means they can be petrochemical, oleochemical or other (that would be coal mainly)

In Asia –Mid-cuts supply seems to be constrained and pricing being forced up – above the ethoxylate price. This seems to be anomalous and reader input is solicited.

A portion of the US fatty alcohol market is served by import and freight disruptions through the Middle East are being felt. Freight rates and lead times are going up. Prices are trending up. Mid-cuts are moving obver USD 2,000 per MT.

In Europe, a similar story, but weaker demand and downward pressure. Midcuts moving up over $1,700 per MT.

AI Corner

This may read like an ad, but it isn’t. I just want to encourage all formulators to sign and use this tool. It will improve your life. No exaggeration.

Potion AI, which was featured in my 7 Most Interesting Companies at InCosmetics video, is enabling some brilliantly interesting insights on their platform that every formulator in your network should get their hands on.

For example, you can figure out in a few clicks that a viral new beauty product, Makeup by Mario's bronzing serum likely uses Croda's Matrixyl 3000 OS in its formula. By using their free AI tools you can conduct similar competitive analysis and also receive unique insights directly to your inbox on a bi-weekly basis.

Once you sign up on their website, you'll receive an email from them with instructions on accessing the platform.

This will be you - except you’ll be wearing safety glasses

Music Section:

I’ve been listening to an eclectic mix this month.

First – Later Zep (that is past IV). Isn’t Achilles Last Stand a masterpiece? Check it out. Love the opening:

And Song Remains the Same off Houses of the Holy

And Physical Graffiti with that super-cool cover and not a bad song on the double album. But check out this absolute monster. Is this not some incredible kind of blues? In My Time of Dying.This song borrows from an old Blues tune of the same name also known as "Jesus Make Up My Dying Bed," which was performed by Blind Willie Johnson in the 1920s. Bob Dylan recorded an adaptation of the song on his first album, which Led Zeppelin used as the basis for their version.

Wow right? – there’s so much more from Zep we could listen to, but actually this month I have spent most of my music-time still down the dub rabbit hole from last month. What an incredible canon of work originating from that small island in that short period of time. It’s like the musical equivalent of 15th Century Florence. Here’s some I’ve really enjoyed the last few weeks.

The sound of Macka Dub

Love these duels…

Check out the flute….

That’s it for this month! Get signed up for the Asian Conference now. See you there in KL - November 20 – 21 (Course on the 19th).